Commissioned by uranium enrichment services provider Urenco, the study - titled A new nuclear world: How small modular reactors can power industry - analyses the energy demands of 11 industries representing 80% of industrial energy use, going beyond data centres to examine where SMRs can make a tangible impact on industrial energy delivery, and quantifies how changes in delivery models and market drivers can expand SMR market access. The report is supported by World Nuclear Association.

"Data centres, chemicals, and coal repowering (i.e., coal-to-nuclear transition) are expected to drive near-term demand, with synthetic aviation fuels representing the largest long-term opportunity," the study says. "Without SMRs, these industrial sectors may face constrained growth or be forced to default to carbon-intensive alternatives due to the lack of clean, reliable energy. Despite this large potential market, only 7 GW would be deployed by 2050 under current deployment trends."

Four supply scenarios are presented: the Current Scenario, which reflects limited deployment based on current supply capabilities; the Programmatic Scenario, which achieves moderate growth through sustained government support and enhanced project management; the Breakout Scenario, which achieves scalable, predictable, and low-cost delivery through shipyard manufacturing; and the Transformation Scenario, with full re-engineering of nuclear technology into a mass-manufactured product, representing approximately 2,300 reactors of 300 MW capacity, where the entire project delivery process is designed for manufacture and assembly.

In addition, for each supply scenario, four demand scenarios are evaluated, reflecting different policy environments and levels of customer value recognition for nuclear energy. These scenarios assess how varying long-term gas prices (Energy Cost scenario), energy security premiums (Security scenario), and different degrees of policy support and decarbonisation commitment (Announced Pledges and Net Zero scenarios) affect the size of the accessible SMR market.

The study found that SMRs are a strong technical match for the energy needs of the industries considered, and could supply up to about 15,000 TWh or 2,200 GW of their demand.

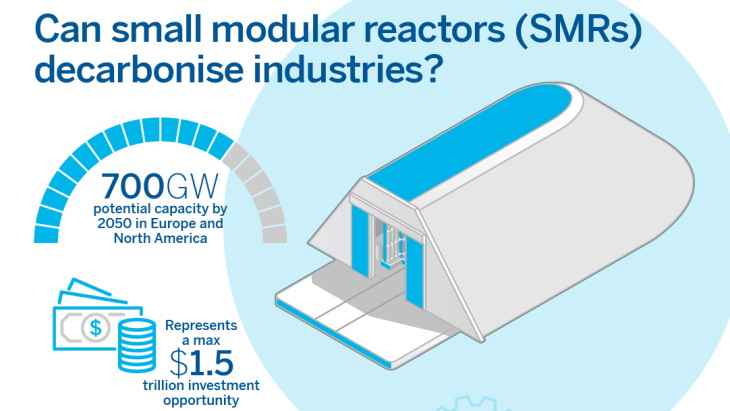

The study also found that manufacturing innovation is key to unlocking the full potential of the SMR market. Improvements to current construction methods (the Programmatic supply scenario) could achieve 120 GW by 2050. However, evolving to full mass manufacturing (the Transformation supply scenario) could enable nearly 700 GW deployment, representing a USD0.5–1.5 trillion investment opportunity.

"This 700 GW of accessible SMR market represents nearly double the current global nuclear capacity, and would expand nuclear capacity beyond the projected goal to triple conventional deployment by 2050," the report says. "The top five SMR accessible markets, representing more than 75% of the 700 GW opportunity, are synthetic aviation fuels (203 GW), coal plant repowering (110 GW), synthetic maritime fuels (90 GW), data centres (75 GW), and chemicals (55 GW). Sectors such as food & beverage (43 GW), iron & steel (33 GW), upstream oil & gas (33 GW), and district energy (33 GW) also represent sizable opportunities, with district energy being particularly relevant in Europe."

It adds: "Serving the 700 GW potential market will require the transformation of the nuclear delivery model from bespoke construction projects to programmatic construction or manufacturing-based delivery. This transformation increases the effective demand for, and the ability to supply, nuclear projects."

According to the study, simultaneous improvement across these Six Critical Market Drivers can enable the evolution of nuclear delivery models and expand market penetration for SMRs: delivery innovation through product-based manufacturing; regulatory evolution toward product-based licensing; economic viability through policy support; site availability through pre-qualification programmes; capital access from mainstream financing; and developer ecosystem maturation with proven delivery track records.

"The gap between today's 7 GW and tomorrow's 700 GW is bridgeable," the study concludes. "The technology exists. The industrial demand is urgent. The policy momentum is building. The delivery models are emerging ... The opportunity is massive. The pathway is clear. The transformation is achievable. The time to act is now."

Urenco Group CEO Boris Schucht said: "Decarbonising industry presents a tremendous challenge that we must all embrace if we are to achieve net-zero by 2050 or sooner. We believe the new-nuclear SMR market holds one of the solutions to this problem: flexible, adaptable, safe technologies that can produce clean energy consistently and affordably. This study acknowledges that with a strong focus on enabling delivery, SMRs can be maximised to their fullest and most competitive potential, significantly enhancing the ability of the nuclear industry to make an important contribution to energy security and net-zero goals."

"We're witnessing a transformation in how nuclear energy services can be delivered to industrial customers," Kirsty Gogan, Managing Partner of Lucid Catalyst, said. "The innovations in manufacturing, licensing, and siting that this study identifies as being critical for enabling scale are already emerging in the market. With the right policy support and industry coordination across six critical areas, small modular reactors can provide a net-zero solution for energy-intensive industries requiring highly reliable, competitive, and scalable, emissions-free heat and power."

King Lee, Head of Policy and Industry Engagement at World Nuclear Association, added: "This study highlights the scale of opportunity for nuclear energy to support decarbonisation of a wide range of industrial sectors. To realise the full potential of nuclear energy would require new regulatory frameworks and production and deployment models to unlock the economy and scale of implementation far beyond current projections."

_20852.jpg)

_59982.jpg)

_64496_89439.jpg)

_90430.jpg)